China

Taiwan reports new large-scale Chinese air force incursion

China is planning to allow the country’s top AI companies to buy a limited number of Nvidia’s, opens new tab H200 chips, the Information reported on Wednesday, citing two people with direct knowledge of the matter.

Chinese officials have told Alibaba, opens new tab, ByteDance and DeepSeek in recent weeks that they may soon receive permission to buy some H200 chips, the report said.

Shares of Nvidia rose 1% after the report.

The chip giant did not immediately respond to a Reuters request for comment, nor did the U.S. commerce department, which oversees exports of advanced AI chips overseas.

China’s commerce ministry also did not immediately respond to a request for comment, while Alibaba, ByteDance and DeepSeek did not respond outside of regular business hours.

The U.S. government has allowed Nvidia to sell its advanced H200 chips to China, and licensed about 10 Chinese firms to buy the chips. However, Chinese officials, keen to nurture domestic suppliers, have withheld approval so far.

Reuters reported in March that Nvidia had won Beijing’s approval to sell the chips to China, citing sources, and around the same time, Nvidia CEO Jensen Huang also told CNBC that the company had clearance from China.

Beijing is still determining the exact number of Nvidia chips to approve, and it could amount to fewer than 200,000 in total, the Information said, adding that was less than half of what the companies requested earlier this year.

Last month, Reuters exclusively reported that Nvidia told Chinese clients its new “Vera” central processors for AI data centres could be available as soon as August and that they can begin placing orders.

Nvidia’s market share in China has effectively fallen to zero, Huang said in October, hurt by U.S. export controls and Beijing’s push for self-reliance in key technologies.

The potential shift in China’s stance underscores the growing computing capacity crunch that the country’s tech companies are facing.

China’s Ant Group said on Saturday that its founder Jack Ma will no longer control the Chinese fintech giant after the firm’s shareholders agreed to implement a series of shareholding adjustments that will see him give up most of his voting rights.

Ma previously possessed more than 50% of voting rights at Ant but the changes will mean that his share falls to 6.2%, according to Reuters calculations.

While Ma only owns a 10% stake in Ant, an affiliate of e-commerce giant Alibaba Group Holding Ltd (9988.HK), he exercised control over the company through related entities, according to Ant’s IPO prospectus filed with the exchanges in 2020.

Hangzhou Yunbo, an investment vehicle for Ma, had control over two other entities that own a combined 50.5% stake of Ant, the prospectus showed.

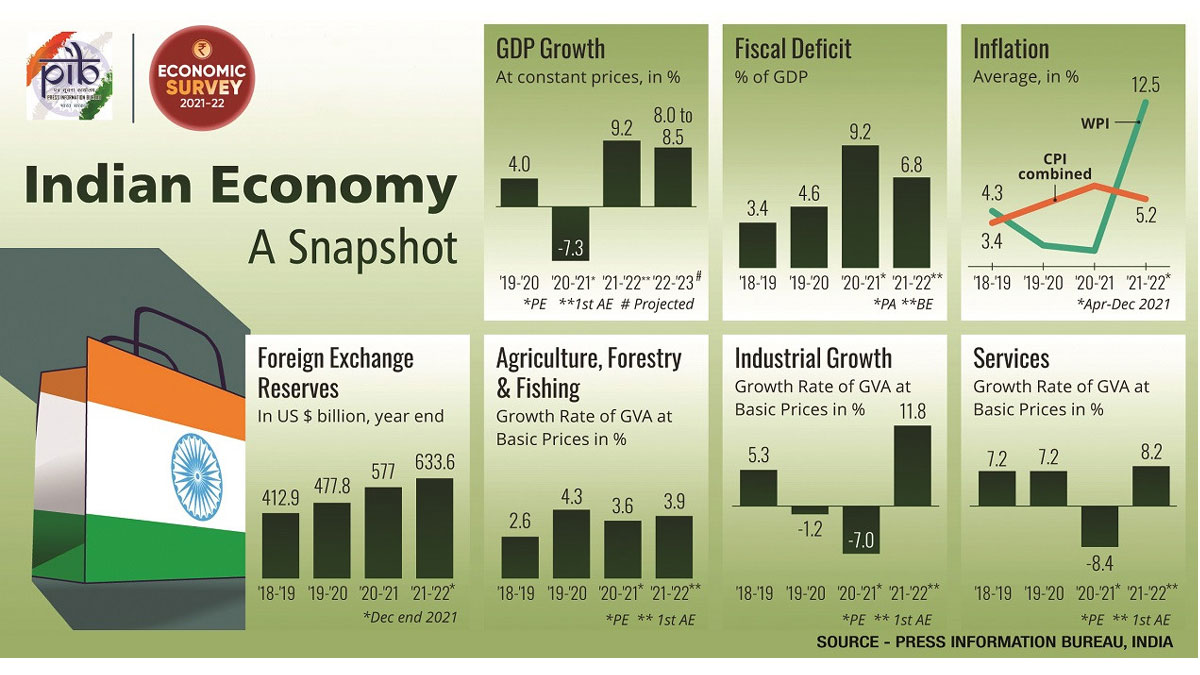

India is going to step up spending to $529.7 billion in the 2022-23 fiscal year to build public infrastructure and drive economic growth to 8-8.5%, as it looks to dethrone China as the fastest growing economy.

Indian Finance Minister Nirmala Sitharaman, while presenting the annual budget on Tuesday, said total government spending in FY23, beginning in April, will be 4.6% more than the current 2021-22 fiscal year.

But inflation poses a major risk for the country in achieving the targeted economic growth rate, according to an economic survey tabled by Sitharaman just a day ago.

There is a threat of imported inflation from the depreciating rupee value against the US dollar and the rising global oil prices that have touched $90 a barrel last week, the survey found.

“Although the high wholesale price index inflation is partly due to base effects and will even out, India does need to be wary of imported inflation, especially from elevated global energy prices,” the survey reads.

The consumer price index (CPI) or retail inflation shot up to 5.59% in December last year from 4.91% in November.

What does high inflation in India mean for Bangladesh?

Zahid Hussain, former lead economist at the World Bank Bangladesh office, said that even before this year’s proposed budget, India’s rising inflation was identified as one of the biggest challenges behind the country’s rapid economic growth.

“I think this inflation will continue even in the third wave of the ongoing coronavirus in the country. And if that happens, it will affect our economy as well. In particular, our import costs may increase slightly,” Hussain warned.

“Our business and economic ties with India are very old. Moreover, the import-export relationship between the two countries is quite strong. Especially our imports from India have been increasing for the last few years,” he told media.

“A recent Policy Times report predicted that Bangladesh would be the fourth largest export destination for India in the current FY22. So, Bangladesh is becoming important for them day by day. However, if this picture of import is different for us, the open market will remain,” the economist also said.

Shahidullah Azim, vice-president of the Bangladesh Garment Manufacturers and Exporters Association (BGMEA), said that Bangladesh imports yarn, fabric, cotton, and some other apparel-related raw materials from India.

“If the inflation rate rises in India, it will have an impact on the overall economic activity of the country. So naturally, there is a strong possibility that the prices of the products we import will go up,” he added.

However, he said, in this global free-market economy, there is no chance of being dependent on any particular country for both export and import.

“If the prices of Indian products go up, we have to find another market to meet our import demand,” he added.

He also said that there are many countries in the world that export RMG related raw materials.

“If the prices go out of our reach, then we have to rush to those countries to find new import sources,” he added.

A director of Savar-based Aboni Fashions Limited also said their factory imports a major portion of yarn and fabric from India.

“Being a neighbouring country, it is quite convenient to import raw materials from India as it saves costs and lead time,” he added.

But if the price of apparel-related raw materials increases due to inflation, it is natural to look for a new market, he added.

In the first seven months of the current fiscal year (April-October of 2021), Bangladesh’s imports from India increased by 81% over the same period of the previous fiscal year, amounting to approximately $7.7 billion.

Spending spree to boost growth in FY23

India will allocate trillions of rupees to expressways, affordable housing and solar manufacturing to put growth on a firmer footing in FY23, the Indian finance minister said while presenting the budget on Tuesday.

Sitharaman said public investment must continue to take the lead and pump prime private investment and demand.

“The economy has shown strong resilience to come out of the effects of the pandemic with high growth. However, we need to sustain that level to make up for the setback of 2020-21,” she said.

She announced spending of $2.68 billion for a highway expansion programme and said 400 new trains would be manufactured over the next three years, reports Reuters.

The fiscal deficit for the current year would be 6.9% of the GDP, slightly more than the 6.8% targeted earlier, the finance minister also said.

For the next fiscal year, the Modi government is targeting a deficit of 6.4% of GDP, hoping to build on higher tax revenues and privatisation of state firms.

Abheek Barua, chief economist of HDFC Bank, told Reuters that the 2022-23 budget finely balanced fiscal retreat with supporting economic recovery.

“It focused on a familiar strategy of driving capital expenditure to drive growth, with the intention of crowding in private investment through higher public spending. Although markets could be disappointed with a higher fiscal deficit of 6.4% of GDP for FY23 than expected, it is perhaps prudent to not undertake aggressive fiscal consolidation at this nascent stage of recovery,” he added.

Christian de Guzman, senior vice president at Moody’s Investors Service, said: “Despite the higher-than-expected growth, we still saw a fiscal deficit that was wider than what was budgeted. That continues to demonstrate the risks that are still ongoing from the pandemic.”

Sitharaman also said the central bank would introduce a digital currency in the next fiscal year using blockchain and other supporting technology.

But India’s central bank has voiced “serious concerns” around private cryptocurrencies on the grounds that these may cause financial instability.

Financial aid for neighbours, Tk345 crore for Bangladesh

Meanwhile, India has also announced a Rs300 crore (approximately Tk345 crore) annual budgetary financial assistance for Bangladesh in FY23, up from the Rs200 crore (Tk230 crore) in the current fiscal year.

It has also allocated Rs200 crore as aid to Taliban-ruled Afghanistan and Rs600 crore to military-run Myanmar.

Nepal will get Rs750 crore as foreign aid from India, the Maldives will get Rs360 crore, Bhutan will get Rs2,266.24 crore, and Mauritius will get Rs900 crore.

Two US soccer team staff members suspended by FIFA for Belgium World Cup game

Inside the Haaland machine

‘Little disappointed in our batting unit’: Miraz rues Tigers’ ODI opener defeat against Zimbabwe

-

Bangladesh2 weeks ago

Bangladesh2 weeks agoData Breaches Expose Millions, Reveal Gaps in Bangladesh’s Privacy Law

-

Business2 weeks ago

Business2 weeks agoIMF lowers 2026 world growth forecast

-

Business2 weeks ago

Business2 weeks agoRyanair loses appeals against Italy’s COVID aid to airlines in EU Court

-

Entertainment2 weeks ago

Entertainment2 weeks agoSummer eye makeup trends every Bengali woman will love

-

Business2 weeks ago

Business2 weeks agoNet forex reserves climb to $27.92b

-

Sports2 weeks ago

Sports2 weeks agoWorld Cup quarterfinals: It’s Messi, Morocco, and 6 teams from Europe. And that’s not unusual

-

Sports2 weeks ago

Sports2 weeks ago‘Little disappointed in our batting unit’: Miraz rues Tigers’ ODI opener defeat against Zimbabwe

-

Bangladesh2 weeks ago

Bangladesh2 weeks agoBIBM study finds uneven anti-money laundering enforcement in Bangladesh